3 Tips Towards a Healthy CGA Program

3 Tips Towards a Healthy CGA Program

The summer is a great time to be under water but it’s never a good time for a gift annuity program to be in that situation. Learn three tips that can help diagnose the health of your CGA program.

Does your station have a CGA program? Well, summer is a great time to conduct a financial health check. An annual stress test is always recommended but here are 3 general questions to help you get started:

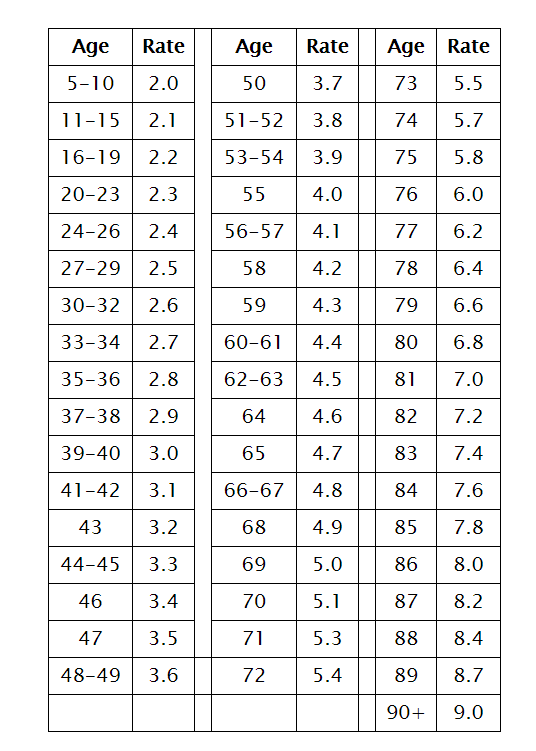

- Are we following the rates suggested by the American Council on Gift Annuities (ACGA)? The rates have been unchanged since January 1, 2012. (See Chart Below). Don’t be tempted to negotiate rates, even when a donor says she can find a better rate with another charity or financial institution. Charities that gamble on life expectancies and financial markets can easily find themselves going underwater quickly. Also remember that a charitable gift annuity is not meant to be competitive with commercial rates. A CGA is first and foremost a gift.

2. How much are we spending on annual expenses? The rates assume a charity is spending no more than 1% of the fair market value of its gift annuity reserve on annual expenses. Relevant expenses include investment and custodial fees, the cost of making payments and filing federal tax forms, and the costs of submitting reports in regulated states. (Minton, Frank, et al. Charitable Gift Annuities, The Complete Resource Manual). Expenses do not include the costs of promoting and obtaining annuity contributions – theses costs are presumed to be covered by your operating budget.

The fixed costs for administration and asset management can pose a serious financial risk for a start-up program. If your station does not have a relationship with a financial institution that will offer you a reasonable rate in the early years, scaling quickly is critical. For example, if your program is spending $20,000 a year from your operating budget to administer and invest a CGA fund with a fair market value of $10,000, you can find yourself in tight spot. A CGA program requires scale to be cost effective. Ideally, the program should be able to pay for itself. For a healthy program, you will need at least $2,000,000 in the fund before you can truly afford $20,000 in annual expenses.

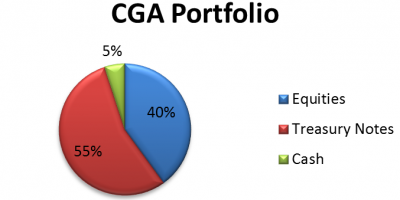

3. What was our return on the investment? Closely monitor the investment return on your reserve fund. The recommended gift annuity rates assume a gross annual return of 4.25%. The segregated reserve fund should be invested in accordance with prudent investment practices. The recommended rates assume a conservative asset allocation:

Pushing more of the portfolio into equities can be tempting, especially in a bull market. However, the market eventually corrects – what goes up often comes down! Think about your long game when it comes to investing. Your goal is to ensure there are sufficient funds to pay the annuitant for the remainder of his or her life and a sufficient residuum is available for the station. Should the fund run dry, the general assets of the station must be used to cover the periodic payments until each contract ends.

Charitable gift annuities can be a great addition to your menu of giving opportunities. Just be sure to keep a close eye on the operation. In the next blog, we will discuss options for CGA programs that are either taking on water or totally submerged. You’ll never know unless you take the time to undergo a thorough health check!

For questions about your gift annuity program, contact Tia J. Graham, Sr. Director, Philanthropy.